If you take both Home and Contents insurance here’s how they can work together if the unexpected occurs:

Plus, you will only have to pay the applicable excess(es) once in respect of any single claim if your buildings and contents are damaged by the same insured event.

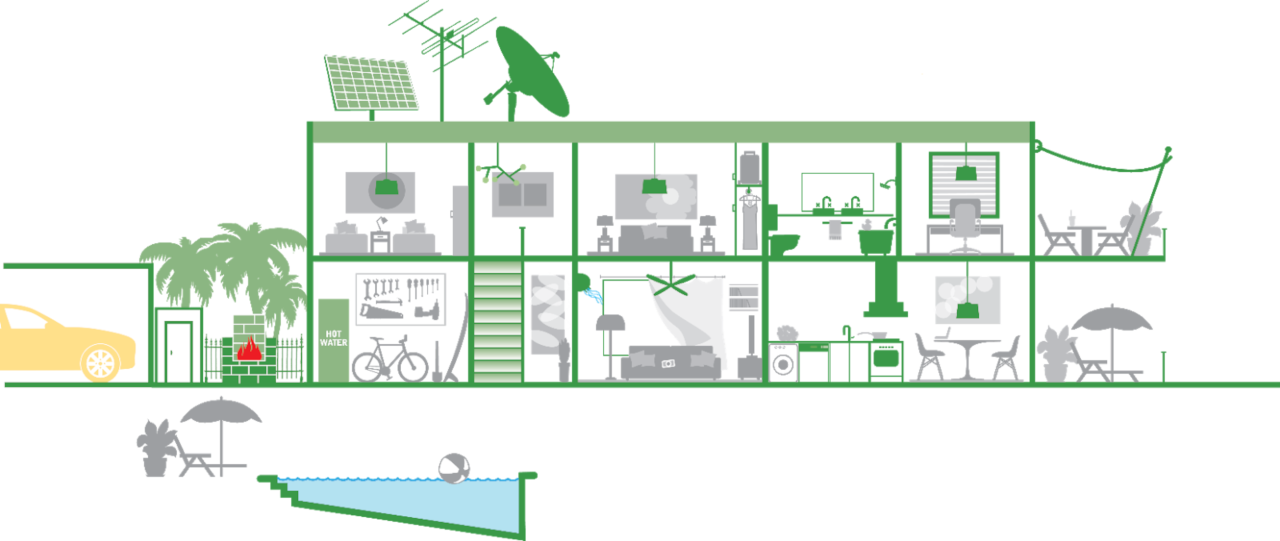

Buildings insurance is designed to insure the physical structures and fixtures that make up your home buildings: from the house itself, to your garage, fences and paved driveways – even built-in appliances like hot water systems, air-conditioners and more.

Contents insurance insures the belongings you have at the insured address: from your furniture, carpet and appliances to your BBQ and even your clothes, shoes and handbags.

So, if any of the insured events happen during the period of insurance, we’ll generally pay to repair or replace your contents – up to the policy limits.

Here is a limited summary of the benefits of a home and contents insurance policy. For full details of the standard terms, conditions, limits and exclusions that apply please read the Home Product Disclosure Statement (PDS) any applicable supplementary PDS before making a decision to purchase the insurance. The Home Buildings and Home Contents key fact sheets also set out some information about the cover.

Home and Contents Insurance |

|

|---|---|

| Rebuilding and professional fees | If you need to rebuild your home after total loss or damage, Allianz will help pay the reasonable costs of architects, engineers, surveyors and solicitors up to $5,000. |

| Cover for the unexpected | Home and Contents Insurance offers protection for out of the ordinary but devastating events such as fire7, storm and burglary. |

| Making your buildings environmentally friendly | If your buildings are totally destroyed and need to be rebuilt, in addition to your buildings sum insured, Allianz will pay up to $5,000 (after deduction of any government or council rebates) to help you make the new buildings more environmentally friendly. |

| Alternative accommodation for you and your pets | If your Building or Contents are damaged by an insured event during the period of insurance to such an extent that you can’t live in your home buildings, Allianz will pay the additional costs for temporary accommodation based on your building’s rentable value prior to the damage, up to 10% of the building or contents sum insured (as applicable) and up to $500 for temporary accommodation for your pets in a commercial boarding establishment. This benefit applies up to a maximum of 12 months. |

| Replacement locks | Home and Contents Insurance pay up to $1,000 to replace the locks or cylinders of any external door or window following an actual or attempted theft or burglary if the key is stolen. |

| Vandalism or malicious damage | Home and Contents will cover you for loss or damage caused by vandalism or a malicious act. |

| Debris removal | In addition to your buildings sum insured, Home and Contents Insurance will pay up to 10% of your home and/or contents sum insured for the removal of debris from the damaged or destroyed part of the buildings. |

| Legal liability | Home and Contents Insurance will cover your legal liability up to $20 million for payment of compensation relating to death, bodily injury or illness, and/or physical loss of or damage to property caused by an accident (or series of accidents). |

| 24/7 claims assistance | When you need to make a claim Allianz are there for you with 24 hour claims lodgement available online, or you can call the claims line to commence the claims process over the phone. |

| Cover when you’re moving house | Home and Contents Insurance will cover your contents for loss or damage caused by an insured event both at your new and old address for up to 14 days after you first start to move. No cover is provided for loss or damage whilst contents are in transit (unless you have Accidental damage cover). |

| Get a quote# | |

Apply to add any of these optional covers for an additional premium and greater cover.

Home and Contents Insurance |

|

|---|---|

| Optional cover – Accidental damage | The accidental damage cover option helps insure you in the event of accidental unexpected mishaps that are caused unintentionally – giving you greater coverage for your home building and/or contents. |

| Optional cover - Portable contents | You can choose optional cover to insure your portable contents such as mobile phones, cameras and engagement rings in the event of theft or an accident at the insured address and when you take them out of your home, even when you are temporarily outside Australia for up to 120 continuous days in any period of insurance. Some portable contents must be specified as Listed portable contents with the full replacement value to be covered away from the home. |

| Optional cover - Motor burnout | The Motor burnout option covers you if an electrical current damages your household electrical motors. This cover is automatically included if you have taken optional Accidental Damage cover. |

| Get a quote# | |

It’s up to you to decide the sums insured, and the type and level of cover that you want to take out. People generally want enough insurance to cover the property’s estimated replacement value. If you don’t have enough cover, you could end up having to cover some of the costs yourself. Remember, Allianz will only pay up to the amount of your loss or the sum insured, whichever is the lesser (subject to the policy terms and conditions) - so you should also be careful not to over insure. That’s why we’ve provided these calculators. They work as guides to help you estimate the replacement value of your home building and contents.

Do what you reasonably can to prevent further loss, damage or liability. Tell the police as soon as reasonably possible about any malicious damage, theft, attempted theft, burglary or loss of insured property. Contact the Claims Call Centre on 13 10 13 and advise the Claims Consultant of what has happened: the Claims Consultant will help you through the home and contents insurance claims process.

In order to be sure that you are covered under this policy you should always contact Allianz for approval before you incur expenses you wish to claim. If you do not, Allianz will pay for expenses incurred to the amount Allianz would have authorised had you asked Allianz first.

If you are altering the security on your property you should inform us as it may change the conditions of your home insurance. This may affect your premium.

You must tell Allianz as soon as reasonably possible if, during the period of insurance you remove or stop using any security devices that were specifically required by us. If you don’t provide this information as soon as reasonably possible, Allianz may refuse or reduce a claim under the policy to the extent Allianz are prejudiced by the delay or the non-disclosure.

You can also contact Allianz if you want to vary your policy during the period of insurance for any other reason, for example to increase your sums insured or to take out additional cover options that may be available.

When Allianz receive this information, Allianz may:

You should tell Allianz as soon as reasonably possible if during the period of insurance your building is in the course of construction or there are any alterations, additions, demolition, repairs to, or decorations of the buildings costing more than $75,000. If you don’t provide this information as soon as reasonably possible, Allianz may refuse or reduce a claim under the policy to the extent Allianz are prejudiced by the delay or the non-disclosure.

When Allianz receive this information, Allianz may:

It is also important that you increase your sum insured to take into account any extensions or renovations to make sure you are adequately covered in the event of a home insurance claim.

You must tell Allianz as soon as reasonably possible if, during the period of insurance you start using any part of your home building for business, trade or professional purposes (except for a home office).

If you don’t provide this information as soon as reasonably possible, Allianz may refuse or reduce a claim under the policy to the extent Allianz are prejudiced by the delay or the non-disclosure.

When Allianz receive this information, Allianz may:

If you’re renting all of your home out to tenants, cover is not available under a Home and Contents Insurance policy. Cover is not available for these types of losses under our home and Contents Insurance. If you rent out part of your home while you live at the same address, please contact us so Allianz can determine if you are eligible for this product.

It’s up to you to decide the sums insured, and the type and level of cover that you want to take out. People generally want enough insurance to cover the property’s estimated replacement value. If you don’t have enough cover, you could end up having to cover some of the costs yourself.

Remember, Allianz will only pay up to the amount of your loss or the sum insured, whichever is the lesser - so you should also be careful not to over insure.

To help you estimate the replacement value of your buildings and/or contents, you can use our Home Buildings and/or Home Contents replacement calculators.

You must tell us as soon as reasonably possible if, during the period of insurance you start using any part of your home building for business, trade or professional purposes (except for a home office).

If you don’t provide this information as soon as reasonably possible, Allianz may refuse or reduce a claim under the policy to the extent we are prejudiced by the delay or the non-disclosure.

When Allianz receive this information, Allianz may:

You can cover laptops, tablets, mobile phones, smart watches and other wearable technology away from the home under the portable contents optional cover. These items must be specified on your policy as Listed portable contents to be covered under this option. Allianz will not cover cracked glass or screens where this is the only damage to the item.

You can apply to add these options to your policy when you start or renew it (or during your period of insurance by contacting Loan Market Insurance on 1800 142 020). If you’re not sure whether you have added these cover options, you can check your policy schedule.

Drones and other remotely or autonomously piloted aircraft used for personal use are covered if lost or stolen within your property.

We do not provide advice based on any consideration of your objectives, financial situation or needs. Terms, conditions, limits and exclusions apply. Before making a decision please refer to the relevant Home Product Disclosure Statement (PDS), any applicable supplementary PDS, and the Home Buildings or Home Contents key fact sheets also available for reference.

#By proceeding with a quote you agree to receive our Financial Services Guide from this website.

Concierge Group Holdings Pty Ltd ABN 95 105 230 046 AR 267687 trading as Loan Market Concierge and Loan Market Insurance arranges this insurance as agent for the insurer Allianz Australia Insurance Limited ABN 15 000 122 850 AFSL 234708. We do not provide any advice based on any consideration of your objectives, financial situation or needs. Terms, conditions, limits and exclusions apply. Before making a decision, please consider the product disclosure statement and key fact sheets available at https://loanmarketinsurance.com.au. The relevant Target Market Determination is available by calling 1300 658 390. If you purchase this insurance, we will receive a commission that is a percentage of the premium. Ask us for more details before we provide you with services.

The Financial Services Guide - Loan Market Insurance can be viewed here.

1. Online Discount

When you both quote and buy a new home insurance policy online a discount of up to 10% is applied to your first year’s premium. This discount is not applied to Domestic Workers’ compensation (if available and selected, not available from 21 December 2025), or upon renewal. Minimum premiums may apply.

2. Combined Discounts

A discount of up to 10% is applied to your premium when you combine Buildings and Contents on one Home and Contents Insurance policy, including the optional covers (if selected): Motor Burnout and Accidental Damage cover. The combined discount doesn’t apply to any flood component of the premium (where covered) or to the optional covers Portable contents (if selected) and Domestic Workers’ compensation (if available and selected, not available from 21 December 2025). Minimum premiums may apply.

3. No Claims Bonus

When you take out a new policy, we calculate your No Claims Bonus (NCB) based on your home or landlord (as applicable) insurance claims history. To qualify for the maximum No Claim Bonus of up to 30%, home insurance customers must have had no Building or Contents insurance claims in the preceding 5 years. Landlord customers must have had no Landlord insurance claims in the preceding 3 years. However, customers who have had claims may still qualify for a reduced No Claim Bonus. We won’t apply the full percentage of the No Claim Bonus if it results in you paying less than the minimum premium.

The No Claim Bonus isn’t applied to the flood component of the premium (if covered) or Domestic Workers’ compensation (if available and selected, not available from 21 December 2025) or Portable contents (if selected).

4. Minimum premiums

Where discounts are applied, your premium is subject to rounding. If more than one discount applies, they’re applied in a predetermined order, so the later discounts apply to the amount already reduced by the earlier discounts instead of the total amount.

Discounts do not apply to government taxes and charges.

Most discounts won’t apply below the minimum amount payable for the policy.

5. Option to change your excess

Not available with respect to any additional compulsory excess, any imposed excess applied to the policy, or to the Portable contents excess (if Portable Contents is selected). Any reduction in premium won’t be applied to government taxes and charges, any flood component of the premium (where covered), or to the optional covers Portable contents (if selected) and Domestic Workers’ compensation (if available and selected, not available from 21 December 2025). Minimum premiums may apply.

6. Instalment premiums

If you choose to pay your premium by instalments you do not pay us any more than if you pay your premium in one lump sum annually. The premiums payable by instalments may be subject to minor adjustments (upwards or downwards) due to rounding. Note: Your financial institution may apply transaction fees to instalment payments.

7. 72 hour exclusion

We may not provide cover for any loss of or damage to your property caused by cyclone, flood, flood water combined with run-off and/or rainwater, grassfires and bushfires during the first 72 hours after you first purchase a policy or increase your cover under an existing policy. Refer to PDS for when exclusion periods apply.